By Nathan C. Goldman and Erynn Stainback

On April 26, 2021, Apple Inc. announced that they would locate a new campus in North Carolina’s Research Triangle Park. Apple’s investment totals approximately $1 billion and will bring in 3,000 new jobs with an average salary of $187,000. Apple’s operational decision represents a significant shift in North Carolina’s, and specifically the Raleigh-Durham metropolitan area’s, economy. In fact, Governor Roy Cooper’s team estimates that this business decision will increase North Carolina’s gross state product by nearly $80 billion over the next 39 years.

The catch comes down to the tax benefits afforded to Apple to entice them to come to North Carolina. Specifically, Apple will receive tax benefits of up to $846 million over the next 39 years as part of the Job Development Investment Grant (JDIG) program. Under the terms of the program, Apple will receive cash grants as reimbursements for the employer’s portion of their employees’ withholding taxes. Apple will need to adhere to strict guidelines, such as their planned new jobs, minimum average wage and capital investment.

While these types of incentive packages are more common as companies expand to new locations – and Apple is not the first, nor the last, to take advantage of North Carolina’s JDIG program – a natural question arises: is it worth it?

To answer this question, Poole College of Management’s assistant professor of accounting, Nathan Goldman, and lecturer, Erynn Stainback, consider the potential incremental tax revenues that Apple will generate with its 3,000 jobs. Their analysis shows that even if you only focus on the additional individual state income taxes collected from the 3,000 new Apple employees in RTP, this deal is a clear-cut win for North Carolina as it would recoup tax revenues otherwise lost with ten years still remaining on their deal.

However, with some simple tweaks and assumptions, Goldman and Stainback provide evidence that the state of North Carolina and local municipalities could recoup the tax breaks in seven years, and in as few as four years.

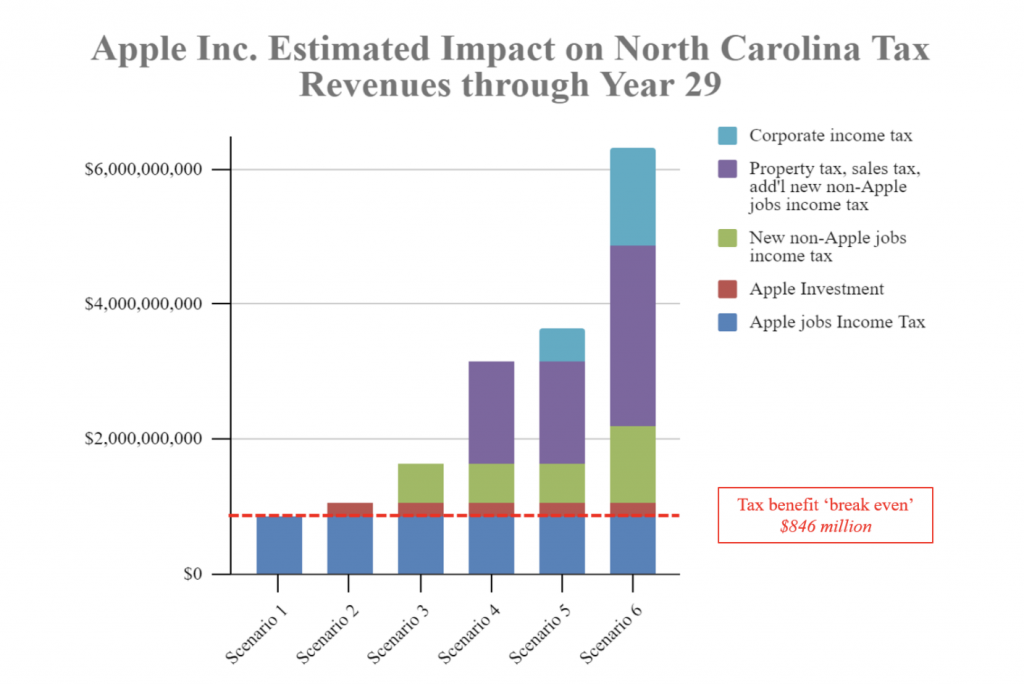

Scenario #1 – Minimum Tax Revenues:

As of 2020, North Carolina’s individual income tax rate is 5.25%. Thus, if we consider the very baseline tax revenues that 3,000 jobs will generate at $187,000 per job, and multiply that income by the 5.25% tax rate, then we estimate that North Carolina will receive an additional $29.5 million in tax revenues per year. This result means that the $846 million in tax benefits would ‘break even’ by year 29.

Scenario #2 – Apple’s Investments

In addition to bringing their facility to North Carolina, Apple plans to spend $110 million in infrastructure in 80 of North Carolina’s counties in the greatest need, and an additional $100 million to support schools and community initiatives. While North Carolina is providing significant tax benefits to Apple over 39 years, North Carolina will also receive more immediate benefits in return based on these investments that would otherwise be funded by the state and taxpayer dollars. If we net these two investments against Apple’s tax benefits, the net cost to North Carolina is actually $636 million. Based on the $29.5 million in tax revenues per year from the calculation in scenario #1, we estimate the ‘break-even’ point is year 23.

Scenario #3 – Non-Apple Jobs

While Apple plans to bring 3,000 jobs to the Triangle, the total economic impact is not limited to those jobs alone. There are many downstream and upstream companies that work closely with Apple that will likely locate operations to some extent in North Carolina to help continue to support Apple’s operations and working environment. While it is difficult to estimate the precise number of additional jobs generated, we conservatively predict that the true increase in jobs is at least double – 3,000 additional non-Apple jobs, with half of those pertaining to high-tech, higher-wage positions (like those that Apple is bringing) and the other half pertaining to support roles that are not earning as high of wages (i.e., office cleaning personnel, restaurant workers, transportation workers, construction workers, among others).

If we expand our model to assume there are 1,500 new jobs in addition to those at Apple making $187,000 ($841.5 million of income) and 1,500 new non-Apple jobs making $60,000 ($90 million of income), then – including everything from Scenario’s #1 and #2 – North Carolina will record approximately $56 million in incremental income tax collections per year. These additional revenues will lower the ‘break-even’ point to 15 years.

Scenario #4 – Other North Carolina Taxes

Income taxes are not the only other source of state tax revenues. In fact, the average sales tax in the surrounding counties (Wake, Durham and Chatham) is 7.17% (4.75% for the state of North Carolina, and an average of 2.42% for the counties). Furthermore, the average property tax in these counties is 0.936%. If we assume that each of the new 6,000 employees has annual expenses subject to sales tax of $12,000 ($1,000/month) and half of these employees purchase a home worth an average price of $300,000, then we can estimate the other North Carolina taxes. Following these assumptions, we estimate that North Carolina and local municipalities will receive approximately $58 million per year in additional tax revenues from these sources. Combining these taxes with the prior scenarios, we estimate a ‘break-even’ point of eight years.

Scenario #5 – Apple’s Corporate Income Taxes

The JDIG program does not exempt Apple from paying corporate taxes in the state of North Carolina (2.5% rate). For the year ending September 30, 2020, Apple had global profits of more than $67 billion. If we assume that 1% of these profits will now be sourced in North Carolina ($670 million), then we estimate that North Carolina will collect an additional $16 million per year in corporate taxes. These additional revenues lower the ‘break-even’ point to seven years.

Scenario #6 – A Less Conservative Estimate

Scenarios #3, #4, and #5 involve conservative estimates. For example, Apple is likely to attract far more than 3,000 non-Apple jobs. Additionally, given that many of these jobs are high paying, the average expenditures and home purchase price may likely be above $12,000 and $300,000, respectively. Lastly, it is not clear what amount of Apple’s profits will be sourced in North Carolina. Considering this will be the company’s east coast hub, it is reasonable that it could be well above the 1% estimated in Scenario #5.

Therefore, if we tweak these assumptions to say that 6,000 additional jobs come to North Carolina (3,000 high-paying tech jobs and 3,000 non-tech jobs), the average expenditures is $18,000 and the average home purchase price is $500,000, and Apple sources 3% of its global revenues in North Carolina, then we estimate the new ‘break-even’ point is just four years.

In other words, the additional tax revenues to the state of North Carolina and local municipalities might be in excess of $200 million additional per year because of Apple.

To help illustrate this impact, we have compiled these scenarios into their total expected economic impact as of Year 29, which is where the State of North Carolina ‘breaks even’ (as indicated by the red-dashed line) on just the income tax collections from Apple’s 3,000 employees alone.

What becomes clear from this illustration is that the tax collections from numerous other sources will lead to gains above and beyond the $846 million provided.

Conclusion

Even using the most conservative set of calculations where we assume the State of North Carolina only benefits from the tax revenues provided by an incremental 3,000 Apple Inc. employees, the state appears to see significant financial benefits from Apple’s presence – even beyond the $846 million in tax benefits.

We caveat these calculations in that there are many underlying assumptions. For example, we calculate everything in terms of 2021 dollars (i.e., no time-value of money), and assume that tax rates remain the same and the 3,000 highly-paid employees will begin working here soon and stay here for this four-decade-long agreement. We also assume that every job that will come to North Carolina will be incremental. However, many of the assumptions (as highlighted in Scenario #6) are conservative. Despite this, even with our more conservative estimates, the state of North Carolina and the local municipalities will greatly benefit in its tax revenues from Apple’s presence in RTP.

One final note, these tax revenues will also correspond with greater costs. With more workers coming to the Raleigh-Durham area, the state of North Carolina and local municipalities will need to keep up with infrastructure, schools, roads and utilities. State budgets will need to increase to match this growth. Given that many of these expenditures can take long periods of time to address (for example, building a new elementary school or expanding a highway takes many years), the state needs to consider these changes today.

Disclaimer: This Poole Thought Leadership article was compiled using publicly available data on the Apple Inc. deal to locate their new facility in North Carolina. All calculations were performed based on numerous assumptions and subject to inherent limitations due to using forward-looking information.

- Categories:

- Series: